What are the two main pension schemes in Luxembourg?

The purpose of this section is to describe the legislation and the mechanism of the statutory old-age pension of the social security system. This involves pensions to employees under the general scheme, i.e. those who contribute to the National pension insurance fund (CNAP).

The general scheme concerns private sector employees, while the statutory schemes are intended for civil servants, local authorities and the Luxembourg national railway company (CFL).

Until 1998, it was customary to speak of the contributory scheme (private-sector employees) and the non-contributory scheme (civil servants and public employees), since in the former scheme the insured, employers and the State pay a contribution calculated on the basis of wages. This contribution largely determines the subsequent benefit, i.e. the pension. Since 1998, however, employees in the second of these schemes have also paid a contribution of 8% on their salary. In fact, their scheme has also become contributory. Therefore, the correct terms are the general scheme for private sector employees and the statutory schemes for civil servants,

municipalities and the CFL.

Indeed, the two laws dated 3 August 1998 – while maintaining the system of pension calculation for retired employees at the time of the implementation of the reform – provide for a transitional phase for active employees, where the “last salary” concept is maintained while reducing the 5/6 ceiling, as well as the implementation of a scheme for future civil servants comparable to that in force for the general pension scheme.

For the general pension scheme, this publication takes into account the latest changes in legislation, in particular the reform law dated 21 December 2012 which came into force on 1 January 2013, and reflects the situation on 1 January 2026.

(Last updated on 19.01.2026)

How is the general scheme financed?

The Luxembourg system, like that of many other countries, functions on a pay-as-you-go basis: not only must annual revenues cover current expenses, but they must also contribute to maintaining a compensation reserve that must be more than 1.5 times the amount of annual benefits. In 2023, the reserve was 4.25 times the annual benefits.

The overall contribution rate is set for each 10-year period of coverage on the basis of a technical balance sheet and actuarial forecasts drawn up by the General inspectorate of social security (IGSS). This constant contribution rate is determined in such a way that the present value of likely income covers the present value of likely expenditures and the increase in the reserve. Every 5 years, the IGSS updates its balance sheet and forecasts. If the overall contribution rate initially set is not sufficient to ensure financial equilibrium, the contribution rate is reset by special law for a new 10-year coverage period.

Pay-as-you-go and funding: what are the issues from a financing point of view?

These two concepts are often used in discussions of pension plans.

A pure pay-as-you-go scheme is one in which the pensions of the beneficiaries, or pensioners, are paid for by the contributions deducted from the payrolls of active workers. In this case, we speak of an intergenerational solidarity, a social contract between working people and pensioners: the working generation pays the pensions of the pensioners.

A funding system is a scheme where the contributions collected are not used to pay the pensions of current pensioners, but are invested in financial markets to earn a return. At the end of the insured person’s working life, the capital accumulated in this way determines the retired beneficiary’s old-age benefit.

The two schemes are not fundamentally different. The pay-as-you-go scheme is based on demographic trends, whereas the funded scheme depends on the return on the financial markets. It should also be noted that this return also depends on changes in demography in the end. The more pensioners there are and the fewer assets there are, the less capital will be invested in the financial markets; because pensioners will tend to sell their financial securities while there will be fewer assets to save and therefore invest their savings.

The undeniable advantage of the pay-as-you-go system is the possibility of introducing social elements, i.e. of adapting pensions to overall changes in wages and the cost of living. This is not possible in the funded system.

(Last updated on 16.05.2023)

What is meant by a pure pay-as-you-go premium?

The pure pay-as-you-go premium is the ratio of annual expenditure to annual contributory income. In other words, it represents the ratio between annual current expenditure and the total of salaries, wages and contributory income at the basis of the annual contribution income of the National pension insurance fund (CNAP). In 2024, this premium amounted to 23.11% and thus remains at a level below the contribution rate set at 24%.

(Last updated on 19.01.2026)

What does the concept of load factor cover?

The load factor is an indicator that is often used in the area of pensions. It refers to the number of pensions per 100 active contributors. Thus, a load factor of 25% means that there is one pensioner for every 4 actively working people. A load factor of 150% means that there are more pensioners than working people (i.e. 1.5 pensioners per working person). In 2023, this coefficient amounts to 43.5%.

(Last updated on 03.01.2025)

What is the replacement rate?

The replacement rate can be defined either as the ratio of a pension to the last income from work at the time of retirement or as the ratio of the average level of a pension during the period it is received to the average level of income during working periods. If a person receives a pension of €2,250 when his last salary was €3,000, the replacement rate is 75%.

(Last updated on 16.05.2023)

What are the sources of funding for the general scheme?

The expenses of the National pension insurance fund (CNAP) are covered mainly by contributions, supplemented by financial and other income. Since 1 January 1985, the overall contribution rate has been set at 24% of professional income with a ceiling. The ceiling is 5 times the social minimum wage.

The 24% is divided as follows: 8% payable by the employee, 8% payable by the employer, 8% payable by the State. For the self-employed, the contribution rate is 16%, corresponding to the insured and the employer’s share, to which is added the 8% payable by the State.

Note: recipients of an old-age pension who are self-employed after the age of 65 are not subject to insurance. If a person receiving an old-age pension takes up paid employment after the age of 65, contributions are due as in the case of liability. In this case, the beneficiary is entitled, upon request, to a refund of the contributions paid after the completion of the 65th year. The refund consists exclusively of the portion of the contributions payable by the insured person and is not adjusted to the cost-of-living index. The refund can be applied for in each calendar year.

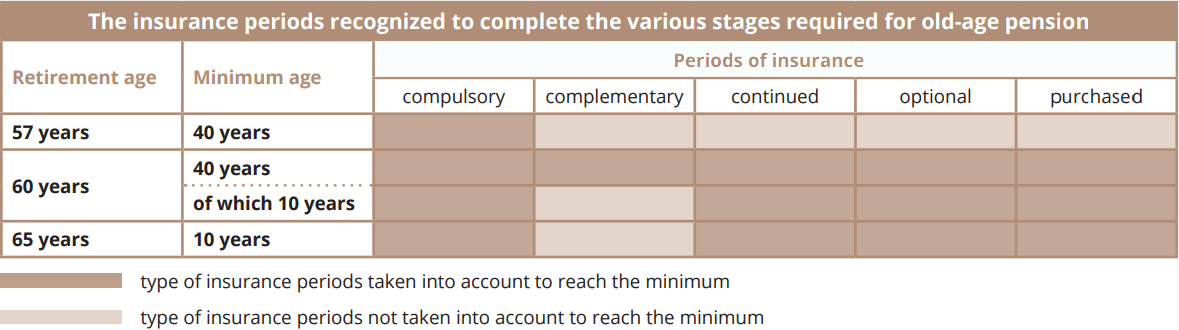

An insured person is entitled to an old-age pension from the age of 65 if he has 120 qualifying months of compulsory insurance, continued insurance, optional insurance or retroactive purchase periods.

(Last updated on 16.05.2023)

What is an early old-age pension?

An insured person is entitled to an early old-age pension from the age of 57 if he has completed 480 qualifying months of compulsory insurance.

An insured person is entitled to an early old-age pension from the age of 60 if he has 480 qualifying months of compulsory insurance, continued insurance, optional insurance, periods of retroactive purchase or complementary periods, including at least 120 qualifying months of compulsory insurance, continued insurance, optional insurance or periods of retroactive purchase.

From July 2026 onwards, insured persons who cannot prove that they have completed 480 months of compulsory insurance will be forced to extend their working life by several months in order to take early old-age pension. Once they have met the age requirement (>60 years) and the contribution period requirement (480 months in total, without having 480 months of compulsory periods), insured persons will have to extend their career by periods of compulsory insurance, continued insurance or optional insurance by:

1 month if they meet the double requirement after July 2026;

2 months if they meet the dual condition in 2027;

4 months if they meet the dual condition in 2028;

6 months if they meet the dual condition in 2029; or

8 months if they meet the dual condition from 2030 onwards.

Extension of insurance periods is not required, either for insured persons eligible for a pension following a period of early retirement compensation for shift workers and night workers or early retirement adjustment, or for employees benefitting of progressive early retirement before 1 July 2026.

(Last updated on 19.01.2026)

What is the difference between an early old-age pension and early retirement?

Many people tend to confuse early old-age pension with early retirement. This confusion arose from the introduction of early old-age pension at the age of 57, which came after the introduction of early retirement, which was also granted from the age of 57.

However, there is a fundamental difference between these two incomes. The old-age pension before the age of 65 falls within the scope of pension insurance, while early retirement, limited to a term of 3 years, is a mechanism to prevent unemployment and is therefore treated as insurance contributions that count toward towards the old-age pension.

There are several types of early retirement:

early retirement due to corporate restructuring (applicable to employees of companies in economic difficulty);

early retirement for shift workers and night workers (applicable to workers who can prove a minimum number of years of work in these conditions);

progressive early retirement (transformation of a full-time job into a part-time job).

The age of early retirement cannot be lower than 57. To be eligible for earl retirement, the employee must be entitled to an old-age pension or an early old-age pension within 3 years.

(Last updated on 16.05.2023)

What are the different insurance periods?

What does compulsory insurance cover?

All persons who carry out a professional activity in Luxembourg for remuneration, either on behalf of another person or on their own account, or who can prove that they have periods of professional activity which are equivalent to such periods, have compulsory insurance under the general pension insurance scheme.

Work performed as seafarers on a ship flying the Luxembourg flag by nationals of Luxembourg or of a country with which Luxembourg is bound by a bilateral or multilateral social security instrument or by persons residing in Luxembourg is treated as an activity in the Grand Duchy of Luxembourg. The same applies to activities carried out as a participant in a peacekeeping operation within the framework of international organisations.

The actual periods of compulsory insurance are periods that count both for entitlement to a pension (stages) and for calculating pensions.

These are periods of professional activity or periods treated as such for which contributions have been paid:

periods of paid employment;

periods of self-employment;

periods for which replacement income is paid on which pension insurance contributions are deducted (sickness, maternity, accident, unemployment and early retirement benefits);

periods of activity carried out by members of religious associations and persons who can be assimilated to them, for the benefit of the sick and of general welfare;

periods of practical apprenticeship corresponding to periods of paid vocational training, provided that these occur after the age of 15;

periods completed by a spouse or partner and, in the case of agricultural activities, by relatives and relations up to and including the third degree of an insured person in a self-employed capacity, provided that the spouse or partner, relative or relation is at least 18 years of age and renders to the said insured person necessary services to such an extent that these services may be regarded as a principal activity;

on request, a period of 24 months or 48 months in the case of parents who devote themselves in Luxembourg to the education of their child or children (baby-years);

Terms and conditions for granting baby-years

The person concerned must provide evidence of a period of compulsory insurance of 12 months during the 36 months preceding the birth or adoption of the child under the age of 4. This reference period is extended insofar as and to the extent that it overlaps with periods during which the person concerned has raised one or more children in Luxembourg.

For cross-border workers, the residence clause is waived in the case where periods of child-rearing are not taken into account by a State other than Luxembourg.

The 24-month period may be extended to 48 months if the person concerned is raising at least two other children in the household or if the child suffers from a permanent reduction in physical or mental capacity of at least 50% compared to a normal child of the same age.

The parents shall designate the beneficiary of the insurance period or, where appropriate, decide to share the period by means of a joint application. This decision cannot be changed. In the absence of an agreement between the parents and in the absence of proof from the claimant parent that he or she has assumed sole responsibility for the child’s upbringing, the said period is shared equally between the two parents.

If a person continues to work full-time during the period in which he or she is eligible for baby-years, the months worked are taken into account as part of the compulsory insurance periods, which take precedence over the upbringing periods. If, before applying for a pension, the same person applies to the pension fund for baby-years, the latter, provided the conditions are met, will be taken into account as “additional notional income”. Pensions will effectively be increased by at least 140 euros per month per child.

Application form available on the National pension insurance fund (CNAP) Website.

periods spent in a developing country as part of development cooperation;

wartime periods for victims of unlawful acts of the occupier;

periods of compulsory military service completed in the Luxembourg army;

periods during which the person concerned has taken part in a peacekeeping operation in international organizations;

periods during which the person concerned was a volunteer in the service of the army;

periods during which a person has provided assistance and care to a dependent person that was not done professionally;

periods during which a person has taken in a child in day and night care, or in day care, and that this care has been provided by an approved entity in accordance with the legislation regulating relations between the State and entities working in the social, family and therapeutic fields;

periods during which the person concerned engaged in a volunteer activity;

periods of parental leave taken by insured persons;

periods during which the person concerned has been engaged in elite sporting activity recognised by the Luxembourg olympic and sports committee;

periods of employment of disabled workers in a sheltered workshop from 1 June 2004;

periods during which a person has received the inclusion allowance under the social inclusion income (subject to prior compulsory insurance contributions lasting 25 years);

periods during which a person has benefited from the severely disabled allowance (subject to prior membership of the compulsory insurance scheme for 25 years).

Periods completed with a view to professional integration or reintegration may also be taken into account.

The following periods shall also be taken into account as periods, but only for the purpose of completing the qualifying stage for the early old-age pension from the age of 60 and for the minimum pension, as well as for acquiring the flat-rate increases, provided that they are not otherwise covered by a Luxembourg or foreign pension scheme:

periods during which a disability pension was paid;

periods of study or vocational training, not compensated as an apprenticeship, provided that these periods are between the ages of 18 and 27. These are secondary, higher or university studies completed in Luxembourg or abroad, evening classes for adults in technical or secondary education, as well as training periods required to obtain a diploma. Interruptions due to illness, holidays and, at the end of the studies, the period between the end of the school year and the following 31 October are considered as equivalent;

the period corresponding to the period of registration required of young jobseekers before entitlement to full unemployment benefits begins;

periods during which one of the parents raised one or more children under the age of 6 in Luxembourg; these periods may not be less than 8 years for the birth of two children, nor less than 10 years for the birth of three children; the age in question is raised to 18 years if the child is physically or mentally disabled, unless the child’s upbringing and maintenance were provided by a specialized institution. Where the country of residence does not grant child-rearing benefits, the country of employment must take account of these periods

if the person concerned was employed or self-employed there on the date on which the child-rearing period began.

With regard to these periods of upbringing, it is presumed that the mother has raised the child. However, the father may provide proof to the contrary:

if he had custody of the child;

if the mother had a professional occupation and the father had custody of the child;

if the father lived alone with the child;

if both parents were working at the same time and the father had the lowest income or, alternatively, was the youngest.

This evidence can only be provided when one of the spouses is eligible for an old-age pension.

periods of insurance corresponding to own-account professional activity exempt from contributions before 1 January 1993;

up to a maximum of 15 years, periods of professional activity in Luxembourg prior to the establishment of the former contributory pension schemes or exempt from compulsory insurance under the legal provisions applicable to these schemes, provided that these periods do not otherwise give rise to benefits and that they occur after the age of 14;

periods from 1 January 1990 onwards during which a person has provided care for the recipient of an attendance allowance, a special allowance for severely disabled persons, an increase in the accident pension for impotence or an increase in the social inclusion income (REVIS);

periods of professional activity subject to insurance under the legislation of the country of origin in the case of persons who, before acquiring Luxembourg nationality, were awarded the status of political refugee and insofar as they are excluded from receiving benefits under any international or foreign scheme;

periods during which disabled workers could not, for reasons beyond their control, be employed in a sheltered workshop, and periods during which the person concerned was unable to earn a living after the age of

18 as a result of physical or mental infirmities; these periods must have occurred before 1 June 2004.

Persons who have 12 months of compulsory insurance during the 3-year period preceding the loss of compulsory insurance status or the reduction in professional activity may apply to continue or supplement their insurance. This 3-year reference period is extended insofar as and to the extent that it overlaps with complementary periods or periods corresponding to social inclusion income (REVIS) benefits or the severely disabled allowance. This application must be submitted to the Joint social security centre (CCSS) 12, under the scheme with which the insured person was last affiliated, within 6 months of losing affiliation.

However, this 6-month period is suspended from the date of application for a disability pension until the date on which the decision becomes final. The continued insurance must cover a continuous period.

Application form available on the Joint social security centre (CCSS) Website.

Persons who do not meet the conditions for admission to continued insurance may, with the approval of the Social security medical board (CMSS), take out optional insurance during periods when they are not working or are working less for family reasons.

Interested parties must:

have been affiliated for effective periods of compulsory insurance for at least 12 months;

not be over the age of 65 or entitled to a personal pension at the time of application.

Under the same conditions, the State shall affiliate persons employed by a Luxembourg diplomatic, economic or tourist representation abroad, provided that these persons are not subject to a pension insurance scheme in another capacity.

Persons who meet the above conditions may take out optional insurance during periods of marriage (or partnership), the upbringing of a minor child or providing assistance and care to a person recognised as dependent by submitting a written application to the Joint social security centre (CCSS) 14. As with the continued insurance, the optional insurance must cover a continuous period.

Application form available on the Joint social security centre (CCSS) Website.

The monthly contribution base may not be less than the monthly social minimum wage, nor more than 5 times this wage.

In the light of these provisions, the person concerned is free to determine the contribution base for continued or optional insurance, which may not exceed the ceiling set at the average (monthly) of the 5 highest annual contributory incomes during the insurance contributions career, increased up to a maximum of twice the monthly social minimum wage, where appropriate.

In the case of continued or optional insurance, the base referred to includes the base of the compulsory insurance.

In addition, the law dated 21 December 2012 on the reform of pension insurance introduced a new minimum monthly contribution base for continued insurance and optional insurance. Accordingly, an insured person can now request that the monthly contribution base be reduced to 1/3 of the monthly social minimum wage for a

maximum period of 5 years under this provision. After the maximum period of 5 years, the insured must again contribute at least the monthly social minimum wage.

On the other hand, the Grand-Ducal Regulation dated 13 March 2013 eliminates voluntary insured contributions for a period of only 4 months per calendar year. The insured person must cover the whole year via a voluntary insurance policy. Nonetheless, a transitional provision provided for by the Grand-Ducal Regulation allows insured persons having taken out non-continued voluntary insurance covering less than 12 months per financial year, before introducing a new option of choosing between maintaining their previous scheme or exercising the new option of 60 months of voluntary insurance on a contribution base of 1/3 of the social minimum wage.

The contributions paid in the context of the continued and optional insurance are tax deductible (article 110 of the amended law of 4 December 1967 on income tax).

What does the notion of purchasing insurance periods cover?

Persons who have either given up or reduced their professional activity for family reasons or left a foreign pension scheme not covered by a bilateral or multilateral social security instrument or a pension scheme of an international organisation providing for a lump-sum redemption or actuarial equivalent may cover or supplement the corresponding periods by a single retroactive purchase over the same period; provided that they have been compulsorily affiliated for at least 12 months and that at the time of application they are neither over the age of 65 nor entitled to a personal pension.

The request for a retroactive purchase of insurance periods must be submitted to the National pension insurance fund, which is responsible for examining the file.

Application form available on the National pension insurance fund (CNAP) Website.

No periods to be covered retroactively may be before the age of 18, nor may they exceed:

periods of marriage or civil partnership;

periods of raising a minor child;

periods of assistance and care provided to a person recognised as dependent or receiving an allowance for care, a special allowance for severely disabled persons, an increase in the accident pension, or an inclusion allowance as part of the social inclusion income (REVIS);

periods of membership of a foreign pension scheme or a pension scheme for an international organisation;

periods which gave rise to payment of the allowance granted to married female civil servants who left the service before becoming entitled to a pension (this provision was eliminated by the law dated 25 July 1985), as well as those provided for by the relevant provisions of the legislation governing other special transitional schemes;

periods of employment with a Luxembourg diplomatic, economic or tourist representation abroad before 1 September 2000.

The National pension insurance fund may ask the person concerned to provide documentary evidence of the above periods. The periods referred to under points 1 to 3 may overlap with periods of compulsory insurance, but the relevant months of insurance are taken into account only once. This also applies to periods completed under a special transitional pension scheme.

How is the assessment base for purchasing periods determined?

For a month of insurance to be covered retroactively during a period referred to in points 1 to 3 and 5 above, at the request of the person concerned, an income is taken into account which corresponds either to the minimum contributory income in force with the National pension insurance fund (CNAP) during those periods, or to multiples of 1.5, 2.0 or 2.5 of that minimum amount. In no case may the income taken into account for compulsory insurance and retroactive purchase exceed the maximum contributory income in force with the CNAP during the calendar year in question.

The amount to be paid for retroactive coverage of insurance periods is calculated on the basis of the above-mentioned income using the overall contribution rate applicable at the time the application is received.

The nominal amount of the contributions thus calculated shall be increased by compound interest at the rate of 4% per annum. The interest shall accrue for each full year from the year following the year to be covered retroactively to the end of the year preceding that in which the application is received. The cost of the contributions shall be shared between the person concerned and the State in the proportion of 2/3 for the person concerned and 1/3 for the State.

The calculation of pension contributions resulting from a retroactive purchase is done using the form available from the CNAP.

The contributions paid in the context of a retroactive purchase are tax deductible (article 110 of the amended law of 4 December 1967 on income tax).

Since the divorce reform and after 1 November 2018 spouses who have taken a break in their career can buy back these years for their retirement, half at the expense of the former spouse; but only under certain conditions.

The legislation now allows that in case of abandonment or reduction of the professional activity by a spouse during the marriage from a period which ends at the latest on the date of the petition for divorce, this person can petition the court to calculate a reference amount for such a retroactive repurchase before the divorce judgement and provided that at the time of the request he/she has not exceeded the age of 65 years, basedon the difference between the respective incomes of the spouses during the period a professional activity was abandoned or reduced.

The spouse who remains active contributes half, provided there is enough money, i.e. within the limits of the assets in joint or undivided property available after payment of all liabilities.

A spouse who has given up or reduced his or her activity may waive this retroactive redemption. This waiver may be made up until the divorce judgment. It may not take place before filing the petition for divorce.

(Last updated on 16.05.2023)

How are the units for calculating insurance periods determined?

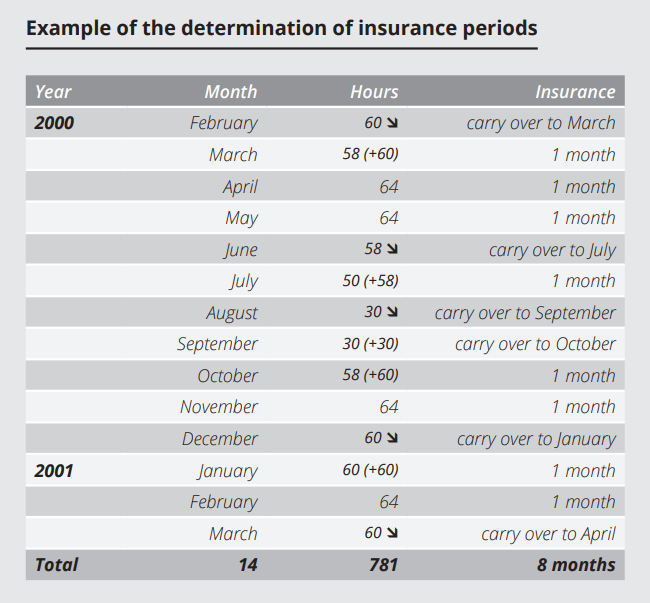

Periods of insurance shall be counted by calendar month. The fraction of a month representing at least 64 hours of work in the case of periods of professional activity exercised for others or periods assimilated thereto, or 10 calendar days in other cases, shall be counted as a whole month. Fractions of months below these thresholds shall be carried over to the following months and taken into account on the first month in which the total number of hours worked, taking into account the carry-over, reaches the said threshold, while wages, salaries and income shall be taken into account for the month to which they relate. However, where various insurance periods are combined (compulsory, continued, optional or retroactive purchase) during one month, the period of crediting may not exceed one month. Where necessary, the months shall be converted into years, the twelfths being converted into decimal numbers.

It should be noted that before 1 January 1988, periods of insurance under the blue collar workers’ scheme were counted in days: the transformation of insurance days into insurance months was then carried out by dividing the total number of days completed by the factor 22.5.

Persons who have received a refund of contributions may reactivate the rights originally attached to the relevant insurance periods by returning the amount of the refunded contributions provided that at the time of the request they are not over 65 years of age and not entitled to a personal pension.

The amount paid back includes the amount of the reimbursed contributions after application of a compound interest rate of 4% per full year, starting from the year following that in which the contributions were reimbursed until the end of the year preceding that in which the contributions were paid back. The amount determined must be paid within 3 months of the notification of the decision or it will be forfeited.

Note, however, that the rights attached to the non-reimbursed portion are reactivated in any case by the completion of a new 48-month period of compulsory, continued or optional insurance contributions.

Refunded contributions are tax deductible (amended law of 4 December 1967 on income tax).

Application form available on the National pension insurance fund (CNAP) Website.

What are the procedures for applying for an old-age pension?

What about entitlement and payment?

The old-age pension begins the day an insured person turns 65 or, if the conditions for entitlement are not met until later, from that subsequent date. An insured person born on 7 May 1949 is therefore entitled to the normal old-age pension from 7 May 2014.

The early old-age pension does not take effect until the day following the expiry of the insured person’s entitlement to his or her occupational income. However, if the insured person remains employed, the pension starts on the first day of the month following the month an application is submitted, but not before the month in which earnings fall below the ceiling set at the average of the 5 highest annual incomes subject to contributions during the insurance period (this ceiling may not be lower than the reference amount plus 50%: €3,961.04 per month on 1 January 2026).

Old-age pensions are paid monthly in advance. Payments are made in euro to 2 decimal places. Payments are transferred to a beneficiary’s bank account with a financial institution. The pension ceases to be paid at the end of the month in which the beneficiary dies. Any overpayments for months after the death must be returned. Any pension arrears relating to a period prior to the death and not yet paid are payable first to the surviving spouse or partner, otherwise to the successors in the direct line of succession up to the second degree, i.e. the children, grandchildren, parents and grandparents.

What are the steps to apply for a resident's pension?

It is important to note that all social security benefits are granted only on approval of a formal application submitted by the person concerned. To avoid unnecessary delays, it is important to submit the application for old-age pension, together with the supporting documents, several months before the date of entitlement to the

National pension insurance fund (CNAP).

The length of time it takes to process pension claims depends on the availability and reliability of basic data and can therefore vary greatly from one claim to another. If, for example, the collection of data involves complex research abroad, the processing may take months. Once the investigation is complete, the pension is approved or rejected by a decision that can be appealed.

Application form available on the National pension insurance fund (CNAP) Website.

What are the procedures for applying for a cross-border worker's pension?

Cross-border workers pay their contributions in the country of their place of work, for example Luxembourg, and therefore benefit from the same rights as resident workers (with the exception of certain non-exportable benefits). In terms of social security, the legislation of the country of employment is applied.

At the time of retirement, all periods of contribution made in a member country of the European Union (EU) or the European free trade association (EFTA, i.e. Iceland, Norway, Liechtenstein and Switzerland) are taken into account and totalled for the purposes of entitlement and calculation of the old-age pension. Each State is therefore obliged to take into account the periods of insurance which were completed in the other countries. It is the principle of aggregation of insurance periods that ensures that periods of insurance or work completed in one State will be taken into account for entitlement to benefits in another State (the rules on aggregation of insurance periods are also applicable under bilateral conventions).

The basic rule is that the insured person wishing to retire submits his or her pension application directly to the competent pension fund in his or her country of residence, which then transfers the liaison forms to the competent bodies in the other countries concerned. However, if the insured person has never worked in his or her country of residence, the claim should be submitted in the country where he or she last worked.

The age of entitlement to an old-age pension is governed by national regulations. This legal age varies from one country to another. The pension of a country is therefore only paid if the claimant fulfils the conditions for entitlement laid down by the legislation of that country. In the event of a mixed career with old-age insurance schemes having different legal ages, insured persons are awarded a partial pension by each country, the amount and legal age of which are determined in accordance with the provisions applicable in the State concerned.

To be entitled to a Luxembourg old-age pension, the insured person must have at least one year of insurance contributions in Luxembourg and at least 10 years of insurance in another country of the European Union (EU) or the European free trade association (EFTA, i.e. Iceland, Norway, Liechtenstein and Switzerland). If the period is less than one year, the months contributed in Luxembourg will be taken into account by the other country and will not give the right to the payment of a Luxembourg pension.

For example, in 2022, an employee was insured for 30 years in Luxembourg, where the pension age is 65, and for 5 years in France, where he is entitled to a retirement pension at 62. If he stops working at the age of 62, he will be entitled to a relatively small pension from France corresponding to the length of the insurance contribution periods completed in that State (5/35). He will then have to wait another 3 years before being entitled to a relatively high pension from Luxembourg (30/35). He will not be able to claim an early old-age pension in Luxembourg from the age of 60 because he will not have a period of insurance contributions totalling 40 years. For the calculation of the 40 years, not only the periods of affiliation completed in Luxembourg are taken into account, but also those completed in France. It is therefore necessary to pay particular attention to this type of situation.

Another example is a cross-border commuter living in Belgium who has worked for 40 years, 30 of which in Luxembourg. In 2022, he can apply for a pension from the age of 57, the minimum age for early old-age pension in Luxembourg. In this case, he will only receive the Luxembourg part of his pension until he reaches pensionable age in Belgium (65 years in 2022).

(Last updated on 16.05.2023)

How does one submit an application?

In principle, social security benefits are granted only after formal submission of an application by the persons concerned. Cross border residents must submit their application to the competent entity in their place of residence, in accordance with the legal requirements of that country. This entity will, if necessary, transfer the liaison forms to the competent entities in the other countries concerned (the insured person must, however, state that he/she has also paid contributions in another country). However, where insured persons have never worked in their country of residence, the application must be submitted in the country where they last worked.

Exemple :

Mr. Doe lived in country A and worked in neighbouring country B as a cross-border worker. He paid pension contributions in country B. There are several possible scenarios:

if he is resident in country A at the time he wishes to claim his old-age pension, he should apply to the body in country A (if he has never worked in country A, the application should be made to the administration in country B);

if he resides in country B, he should contact the administration in country B where he paid his pension contributions;

if he lives in another country (i.e. neither A nor B), he should submit his claim to the pension administration in country B where he was last employed. The latter will forward the claim to the other administrations concerned.

In order to avoid unnecessary delays, it is important to submit the application for an old-age pension to the competent administration well before the date of entitlement.

By way of exception to the principle described above, at the time of retirement, a Belgian, German or French resident who receives sickness benefits from the Luxembourg fund may submit his application for retirement to the competent Luxembourg pension fund. If the cross-border worker is also affiliated in his country of residence, the Luxembourg pension fund will then contact the competent pension administration in the country of residence with a view to examining the pension rights in that country.

(Last updated on 16.05.2023)

How is the pension paid out?

There are three possible scenarios:

if a cross-border worker has contributed for less than a year in the Grand Duchy of Luxembourg and the rest of his career in the country of residence, the pension fund of that country will pay his full pension;

if a cross-border worker has spent part of his professional career in Luxembourg and the other part in the country of residence or in another EU or EFTA country, this is known as a “mixed” career; such workers receive a pension from each State, provided that they have been insured in the country for at least one year;

if a cross-border worker has spent his entire working life in the Grand Duchy, his entire pension is paid by the Luxembourg fund, even if he does not live in the country.

(Last updated on 16.05.2023)

How is the pension calculated?

In the case of a career in only one country, the amount of the pension shall be determined in accordance with the provisions applicable in that State.

In the case of a so-called mixed career, claimants receive a pension from each state in which they paid contributions. The amount of each pension to which cross-border workers are entitled is proportional to the number of years of contributions completed in the country concerned.

Each State where a cross-border worker has been insured shall make the following calculation:

public pension: calculated on the basis of national legislation, taking into account only periods worked in the country for more than the minimum contribution period;

theoretical amount: the competent administration calculates the theoretical amount of the old-age benefit which would have been due if the insured person had completed all periods of insurance, including those abroad, under its legislation (for periods of insurance abroad, the annual average of wages, salaries or contributory income received in Luxembourg is used as a reference by the Luxembourg fund);

proportional pension: on the basis of the theoretical amount, it sets the actual amount in proportion to the length of the insurance periods actually completed under its legislation.

The competent pension fund then pays the higher of the two pensions, usually the proportional pension (this situation only applies in the case of independent entitlement, i.e. when the national periods alone give entitlement to the pension).

Exemple :

The insurance period of an insured person is as follows:

France (FR): 3 years

Belgium (BE): 32 years

Luxembourg (LU): 5 years

Total: 40 years

The proportion allowing the transition from the theoretical amount to the amount actually payable by Luxembourg is therefore equivalent to the following fraction:

LU periods / (LU periods + FR periods + BE periods) = 5/40 = 0.125

As a result, all pension elements determined by totalling up all periods (notional amount) will be multiplied by the pro rata factor calculated in this way.

(Last updated on 16.05.2023)

What remedies are available?

Every application for a pension is approved or rejected by an executive decision taken by the National pension insurance fund (CNAP).

In the event of disagreement, the person concerned may lodge an objection against the decision, which will be decided by a CNAP Board of Directors ruling. The decision of the Board of Directors may be appealed to the Social security arbitration tribunal. An appeal does not suspend enforcement.

If the Arbitration Tribunal finds the claim for pension to be well-founded, it determines the starting point of the pension. As soon as the decision awarding the claim in principle has become final, CNAP determines the amount of the pension. The Arbitration Tribunal will decide in the last resort up to the value of €1,250 and on appeal when the value of the dispute exceeds this sum.

An appeal against the judgement of the Social security arbitration tribunal may be lodged with the High council of social security. The appeal has suspensive effect.

All appeals must be made in writing within 40 days of the notification of the CNAP’s decision or judgment. After this period, the appeal is no longer admissible and the decision becomes final.

It should be noted that insured persons receive an annual statement of their Luxembourg insurance career, provided that they were affiliated during the previous year. They are advised to check the accuracy of this statement.

The annual old-age pension consists of proportional and flat-rate increases. The flat-rate increases are granted on the basis of the length of insurance, the proportional increases are granted on the basis of a contributory element including professional income earned during the insurance period.

The pension is supplemented by an end-of-year allowance.

Pensions are first calculated using the index number 100 of the cost of living on 1 January 1948 and the base year 1984. This makes it possible to compare the salaries of the different years. Once this step has been completed, the pensions benefit from a double adjustment. They are adapted to real trends in salaries (revaluation and readjustment) and to the cost of living (indexation).

The flat-rate increases are granted on the basis of the length of insurance periods and are independent of the insured person’s income level. To calculate this period, periods of compulsory insurance, continued insurance, optional insurance, periods of retroactive purchase and complementary periods are taken into account.

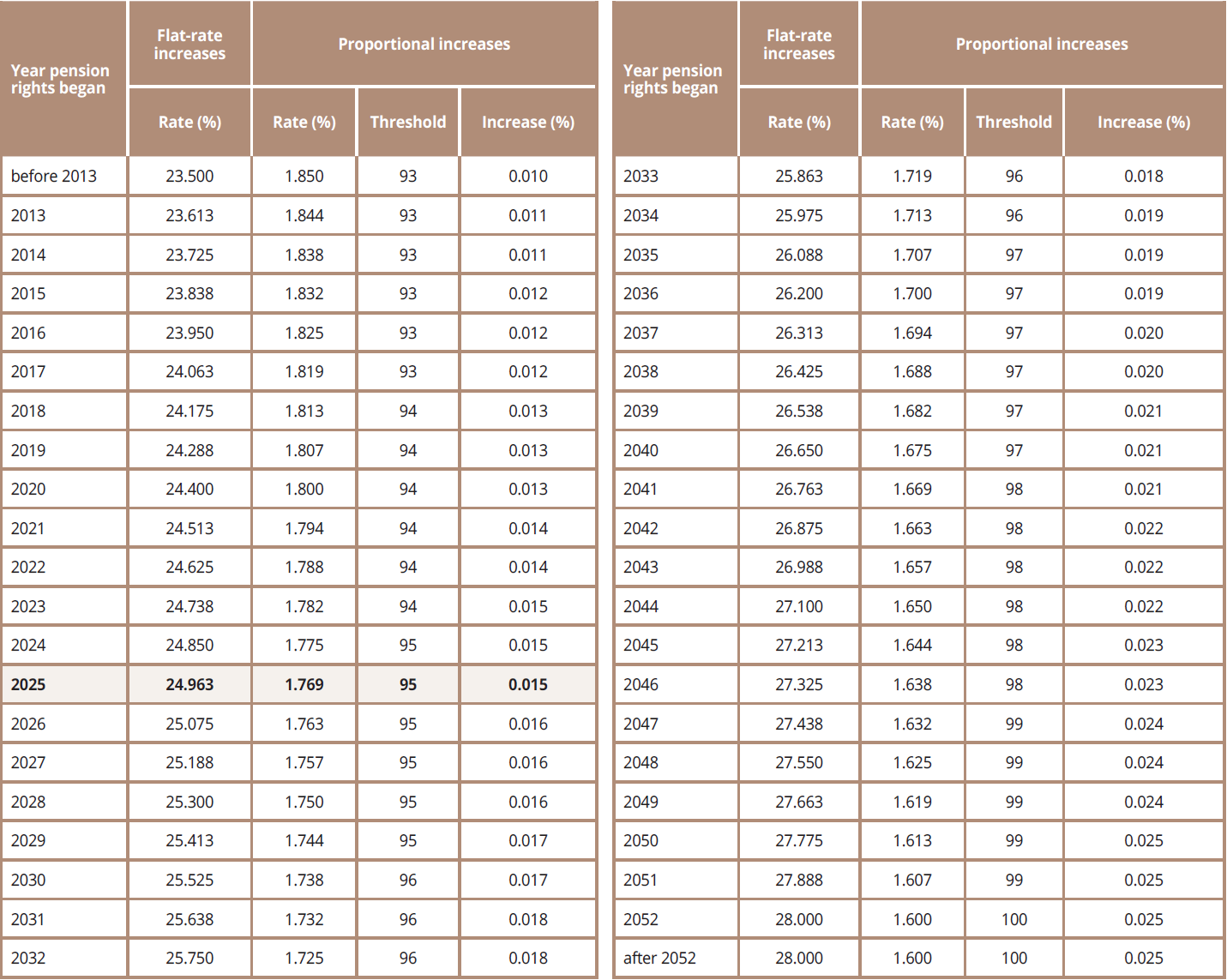

Before the 2012 reform, the amount of the flat-rate increases for an insurance period of 40 years (480 months) was 23.5% of the reference amount. The latter is a parameter used to determine certain thresholds in relation to the calculation of pensions. It is set, at the number 100 of the cost-of-living index on 1 January 1948 and for the base year 1984, at €2,085 per year.

However, the law of 21 December 2012 provided for a gradual increase in the flat-rate increases depending on the year of retirement. In 2026, the amount of the flat-rate increases for a full career (40 years) amounts to 25.075% of the reference amount, and will reach 28% in 2052. This amount is identical for each insured person.

The flat-rate increases are acquired by 1/40 per year, completed or begun, with a limit in the number of years taken into account of 40.

Accordingly, an insured person who retires in 2026 and has 33 years and 3 months of insurance with the National pension insurance fund (CNAP) will obtain flat-rate increases equal to 34/40 of €522.81, which is equivalent to €444.39 per year (at the index number 100 of the cost of living on 1 January 1948 and the base year 1984; this corresponds, on 1 January 2026, to €6,753.94 per year or €562.83 per month at index number 968.04 and revaluation factor 1.57).

Another insured person who has 43 years of insurance in 2026 will receive a flat-rate annual increase of €522.81 (based on the cost-of-living index of 1 January 1948 and the base year 1984; this corresponds to €7,945.84 per year or €662.15 per month as of 1 January 2026, based on index number 968.04 and revaluation factor 1.57).

(Last updated on 19.01.2026)

What do the proportional increases cover?

Proportional increases are calculated by multiplying a percentage rate (which changes depending on the year of retirement) by the sum of the wages, salaries or contributory earnings taken into account.

Before the reform brought about by the law of 21 December 2012, this percentage rate was set at 1.85. However, the new law provides for a gradual reduction of this rate from 1.85 to 1.6% by 2052. For a person whose pension entitlement begins in 2026, this rate is already only 1.763%. For those retiring in subsequent years, the rate gradually decreases to 1.6% in 2052.

To obtain the sum of salaries, wages and contributory income used to calculate pensions, these are reduced by calendar year to the number 100 of the weighted cost of-living index as at 1 January 1948 on the basis of the weighted annual average of the monthly consumer price indices.

These amounts are then brought up to the standard of living of a base year which is 1984. For this purpose, they are divided by revaluation factors that express the relationship between the average gross wage level of each calendar year and that of the base year.

For baby-years, the monthly average of the contributory earnings credited for periods of compulsory insurance during the 12 insurance months immediately preceding the month of childbirth or adoption is taken into account, after deduction of the contributory income credited for the benefit of the persons concerned on another basis. This average may not be less than €270.28 per child per month at the index number 100 of the cost of living on 1 January 1948 and the base year 1984 (€4,235.98 on 1 January 2026).

(Last updated on 19.01.2026)

What is meant by a staggered increase in the proportional increases?

The staggered increase in proportional increases is conditioned by two criteria: age and length of compulsory insurance periods.

The law of 21 December 2012 redefines the conditions for granting and the level of staggered proportional increases. Instead of setting, as before, the beginning of the staggered proportional increases at 55 years of age and 38 years of career, their granting is now subject to a single minimum threshold condition, equal to the sum of age and compulsory insurance periods, which changes according to the year of retirement. This threshold was 93 in 2013 and will gradually reach 100 in 2052.

The rate of staggered proportional increases is gradually increased by year of retirement: from 0.011% per additional year (above the threshold described above) in 2013 to 0.025% in 2052.

In specific terms, the increase in the rate of proportional increases is calculated on the basis of the difference between the age of a beneficiary increased by the number of years of contributions (only the whole years for the actual compulsory insurance periods) and the reference threshold (set at 95 for the year 2026). Accordingly, for

each unit exceeding this threshold, an increase in the rate of proportional increases is provided for (of 0.016% for the year 2026). However, the rate of increase may not exceed 2.05% in total.

While the new formula provides more significant staggered proportional increases than that under the former legislation, the conditions for granting them are also increasingly restrictive over time. For example, in 2052, an insured person aged 60 with 40 years of service will no longer be able to benefit from the staggered increase

(40 + 60 = 100).

Example

In 2026, an old-age pension applicant, aged 60, with 40 years of contributions gets:

60 + 40 = 100 100 – 95 = 5 5 x 0.016% = 0.08% increase in the rate of proportional increases, which thus amounts to 1.763% + 0.08% = 1.843%.

In contrast, in 2052, a pensioner of the same age (60) and with the same length of contribution (40) will not get any increase in the rate of proportional increases. The threshold will be set at 100 (100 – 100 = 0).

(Last updated on 19.01.2026)

How are the flat-rate increases, respectively the rates, thresholds and increases in the proportional increases determined, depending on the year of entitlement?

(Last updated on 22.01.2025)

What is the end-of-year allowance?

The law of 28 June 2002 introduced an end-of-year allowance for people who are entitled to a pension on 1 December.

For beneficiaries of an old-age, disability, spouse’s or surviving partner’s pension, the allowance is equivalent to €1.67 for each year of insurance, completed or begun, under compulsory insurance, continued insurance, optional insurance, retroactive purchase of insurance periods or complementary periods, with a limit in the number of years taken into account of 40. This amount corresponds to the number 100 of the weighted costof-living index as at 1 January 1948 and the base year 1984. It is adjusted to the standard of living and revalued and readjusted.

A pensioner who has completed 40 years of insurance is therefore entitled in December 2026 to an allowance of €25.38104 per recognised year of insurance, i.e. an annual allowance of €1,015.24.

For recipients of an orphan’s pension, the allowance is 1/3 of the allowance previously determined. It is 2/3 for orphans of both parents.

This allowance shall be divided, where appropriate, between two or more surviving spouses, divorced spouses or surviving partners in accordance with the provisions in force for survivor’s pensions (determination in proportion to the duration of the marriages or partnerships and the length of time spent in the household 31).

The allowance is also granted to parents and relatives in the direct line, to relatives in the collateral line up to the second degree and to adopted children who are minors at the time of adoption.

If a pension is not paid to a recipient for the entire calendar year, the allowance is reduced to 1/12 for each full calendar month no pension is paid. The surviving spouse or partner who lived in domestic partnership with the recipient of an old-age or disability pension is entitled to the full allowance for the period of the calendar year

up to the end of the month of death.

The amount of the allowance shall not be taken into account in applying the stipulations relating to the combination of pensions with other income, but it shall be reduced to the same extent as the pension by the effect of those stipulations.

The law of 21 December 2012 now provides that continuation of the end-of-year allowance is linked to the financial situation of the pension scheme. Thus, if the overall contribution rate for pension insurance exceeds 24%, the end-of-year allowance is not due.

(Last updated on 19.01.2026)

What is covered by the double adjustment of pensions?

Pensions are adjusted in two ways. They are adapted to the real evolution of salaries, through revaluation and readjustment and they are adapted to the cost-of-living index, i.e. to the consumer prices, through indexation.

(Last updated on 16.05.2023)

How is the indexing done?

Pensions calculated at 100 of the weighted cost-of-living index as of 1 January 1948 are adjusted by the sliding scale mechanism (index brackets), as are wages and salaries.

Currently, the applicable index number is 968.04.

(Last updated on 19.01.2026)

How is the revaluation and readjustment carried out?

The law of 21 December 2012 introduces a differentiation between the salary revaluation mechanism, i.e. the updating of salaries recorded in the career in base year value 1984 to the level of salaries in the economy at the time of the pension calculation and the readjustment mechanism which consists of annual adjustments of the level of pensions to changes in salaries during retirement.

Revaluation

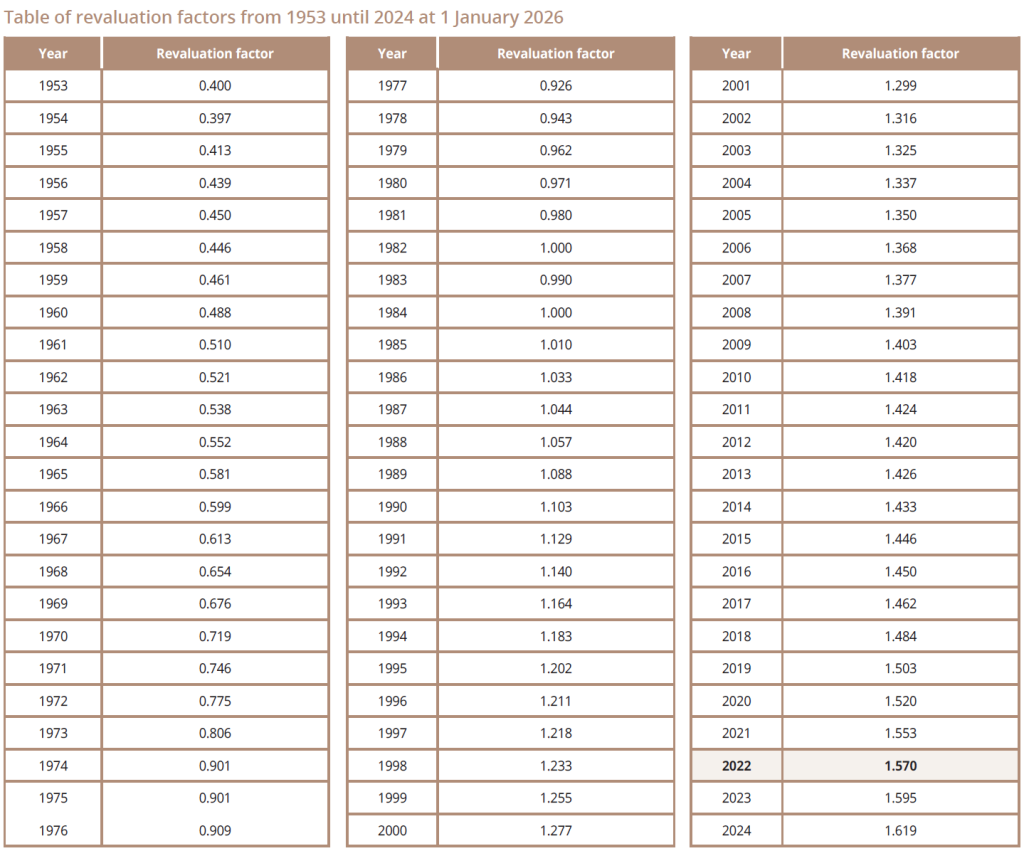

Concerning the revaluation at the time of the granting of the pension, the new law stipulates that pensions whose entitlement starts before 1 January 2014 are multiplied by the revaluation factor, which is set at 1.405. Pensions whose entitlement starts after 31 December 2013 are multiplied by the revaluation factor of the 4th year before the entitlement starts. This revaluation factor is fixed by Grand-Ducal regulation.

In concrete terms, in calculating the pension of an insured person who leaves working life in 2026, the 2022 revaluation factor of 1.57 is applied.

Example of the revaluation of a pension for an insured person who retires on 1 January 2026 at the age of 60

Let us assume that this person’s annual pension based on 1984 at index 100, calculated on 1 January 2026, is €3,000.

This amount of €3,000 must be multiplied by the applicable revaluation factor and the index, i.e.:

3,000 x 1.57 x 9.6804 = €45,594.68 per year, i.e. a monthly amount of €3,799.56.42 on 1 January 2026.

This amount is vested. This means that even if the adjustment shrinks, this pension amount cannot be touched. However, future growth in this pension depends on how real wages increase and the relationship between the pure pay-as-you-go premium and the overall contribution rate.

Readjustment

As for the readjustment of pensions during retirement, the law of 21 December 2012 provides for a new mechanism so that the adjustment of pensions to real wages is no longer automatic and depends on the financial situation of the pension scheme. If the pure pay-as-you-go premium exceeds the overall contribution rate, a moderating mechanism is triggered and the readjustment of pensions during the course of liquidation will be, at most, equal to half of changes in wages.

Specifically, the pensions to which the revaluation mechanism described above has been applied are multiplied by the product of the various readjustment factors determined by calendar year, starting from the year after the start of the pension entitlement (but from 2014 at the earliest).

For a calendar year, the readjustment factor is obtained by adding 1 to the product of the multiplication of the annual rate of change of the readjustment factor between the penultimate year and the year preceding it, and the readjustment moderator applicable for the penultimate year.

The reform law of 21 December 2012 initially set this readjustment moderator at 1. Every year, the government shall examine whether or not to revise the readjustment moderator by legislative means. If the pure pay-as-yougo premium for the penultimate year preceding that of the revision exceeds the overall contribution rate, the Government shall submit a report to the Chamber of Deputies accompanied, if necessary, by a bill setting the readjustment moderator at a value less than or equal to 0.5 for the years from the year preceding the revision.

However, the readjustment moderator may again be increased to a value not exceeding 1 for the years from the year preceding the revision, if the overall contribution rate for the penultimate year preceding that of the revision exceeds the pure pay-as-you-go premium.

The pure pay-as-you-go premium represents the ratio between the annual current expenditure and the total wages, salaries and income base for contributions to the annual revenue of the National pension insurance fund (CNAP). A Grand-Ducal regulation sets the pure pay-as-you-go premium for the previous year.

Example of a 1 January 2026 readjustment of a pension for an insured person who retired on 1 January 2025

Let’s assume that an insured person receives a monthly pension of €3,000 from 1 January 2025.

2026 readjustment factor:

1 + (variation between 2024 revaluation factor and 2023 revaluation factor) x moderator

The revaluation factor is set by grand-ducal regulation; for 2023 it is 1.595 and for 2024 1.619. This represents an increase of 1.5%.

The readjustment moderator for 2025 remains at 1.

1 + 0.015 x 1 = 1.015

In 2026, our insured’s pension will therefore be €3,000 x 1.015 = €3.045.

To this, of course, we must add the index pay-outs.

(Last updated on 19.01.2026)

How is an old-age pension calculated?

Theoretical example of the calculation of an old-age pension

The annual pension is calculated at the index number 100 of the cost of living, taking 1984 as the base year. This pension is then adjusted to the cost of living through indexation and brought up to the standard of living by multiplying it by the revaluation factor. In the following example, the calculation was made on 1 January 2026 (index number 968.04 and revaluation factor 1.57).

Mrs Weber was born on 15 May 1961. She continued her education until May 1981. She began working on 1 May 1981, and continued working until 1 September 1988. On that date, she gave up working because she wanted to take care of her children.

She raised her 2 children, born on 20 June 1988 and 13 October 1989 respectively. On 1 June 2004, she resumed her professional activity, but she stopped working on 31 December 2010.

On 15 May 2026, Mrs Weber is indeed entitled to an old-age pension, as she meets the qualifying condition of 120 months of compulsory membership due to an employed activity. Indeed, these periods of affiliation are as follows:

from 01.05.1981 to 01.09.1988: 88 months from 01.06.2004 to 31.12.2010: 79 months

In addition, since the law of 28 June 2002, baby-years are also granted for children born before 1 January 1988.

Also, until September 1988, Mrs. Weber was on maternity leave. From 1 October 1988, she benefited from baby-years, but only until the youngest child reached the age of 2, in October 1991. This gives her 38 months of baby-years.

Total: 88 + 79 + 38 = 205 months.

The following shall also be taken into account for flat-rate increases:

periods of study or vocational training, provided that these periods are between the ages of 18 and 27. In Mrs Weber’s case, this means 24 months (the period between 15.05.1979, when she reached the age of 18, and 01.05.1981, when she completed her studies);

the periods of education of children under 6 years of age. This is the period of time between the birth of the first child (20.06.1988) and the date when the second child was 6 years old (i.e. 13.10.1995). This is equivalent to a total of seven years and 5 months. However, for 2 children, the total periods cannot be less than eight years. Ms Weber already benefits from 38 months under the heading of baby-years. She is therefore still entitled to 58 months of child-rearing periods (96 – 38 months).

If Ms. Weber retires in 2026, the total of compulsory and complementary insurance periods counting for the stage of an old-age pension at the age of 65 and for calculating the flat-rate increases will be:

205 + 24 + 58 = 287 months / 12 = 23.92 years, which is rounded to 24 years.

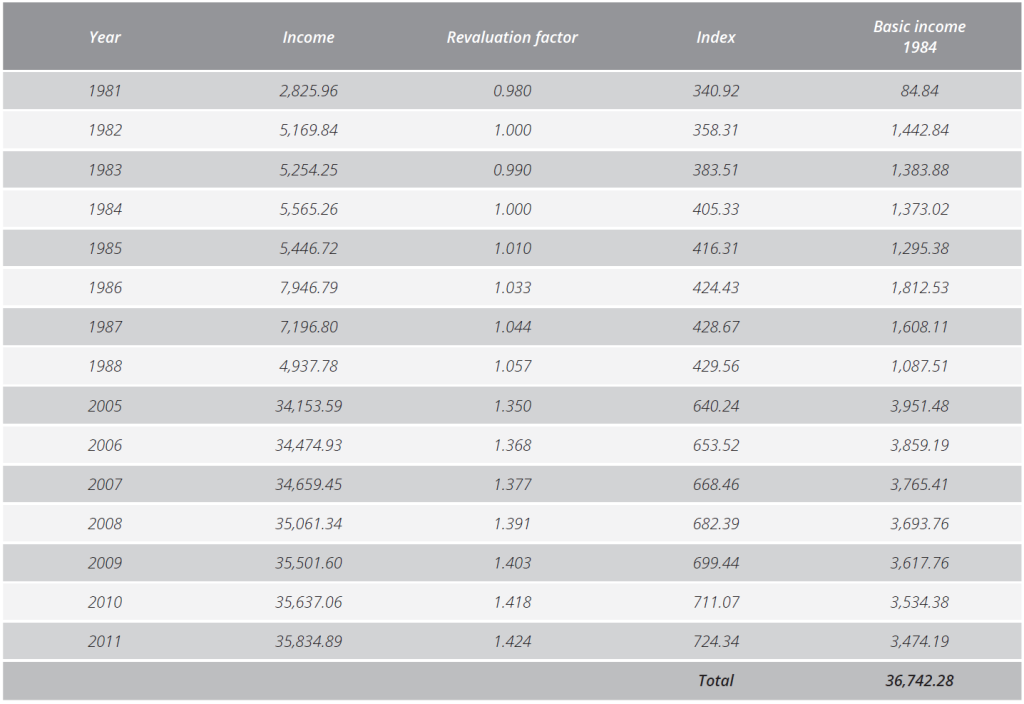

Ms. Weber’s compulsory insurance period earnings are as follows:

Explanation: for each year, we take the income (in euros) received by Ms. Weber, divide it by the revaluation factor to bring it back to the 1984 base and divide it by the index to bring it back to index 100. At the end, we calculate the sum of all the annual incomes.

In addition to these incomes, we have to take into account the baby-years. Let’s assume that before the birth of her first child, Mrs Weber had an average monthly income of €109.03 based on the cost-of-living index of 1 January 1948 and the base year 1984. However, the Social Security Code stipulates that the income may not be less than €270.28 per child per month, still based on the cost-of-living index of 1 January 1948 and the base year 1984.

It is therefore necessary to add for the 2 children: 38 x €270.28 = €10,270.64

The amount entered in the accounts for proportional increases is therefore:

€36,742.28 + €10,270.64 = €47,012.92

To determine Mrs Weber’s pension, the amount for the base year 1984 is first calculated:

Mrs Weber receives 24/40 of the flat-rate increases, i.e. 24/40 of 25.075% of €2,085, or €313.69.

To this must be added the proportional increases, i.e. 1.763% of €47,012.92, or €828.84.

The annual pension based on 1984 at index 100 is therefore €313.69 + €828.84 = €1,142.53.

Per month, this is equivalent to €1,142.53/12 = €95.21 index 100.

To get the monthly pension amount at the 2026 standard of living and the current index, it must be multiplied by the corresponding revaluation factor and index.

As of 1 January 2026, the applicable revaluation factor is 1.57 and the index is 968.04.

Mrs Weber’s monthly pension is therefore: €95.21 x 1.57 x 9.6804 = €1,447.02.

(Last updated on 19.01.2026)

How is an early old-age pension calculated?

Theoretical example of the calculation of an early old-age pension

As in the previous example, the annual pension is calculated at index 100 of the cost of living and using 1984 as the base year. This pension is then adjusted to the cost of living through indexation and brought to the standard of living by multiplying it by the revaluation factor. In the following example, the calculation was made on 1 May 2026 (index number 968.04 and revaluation factor 1.57).

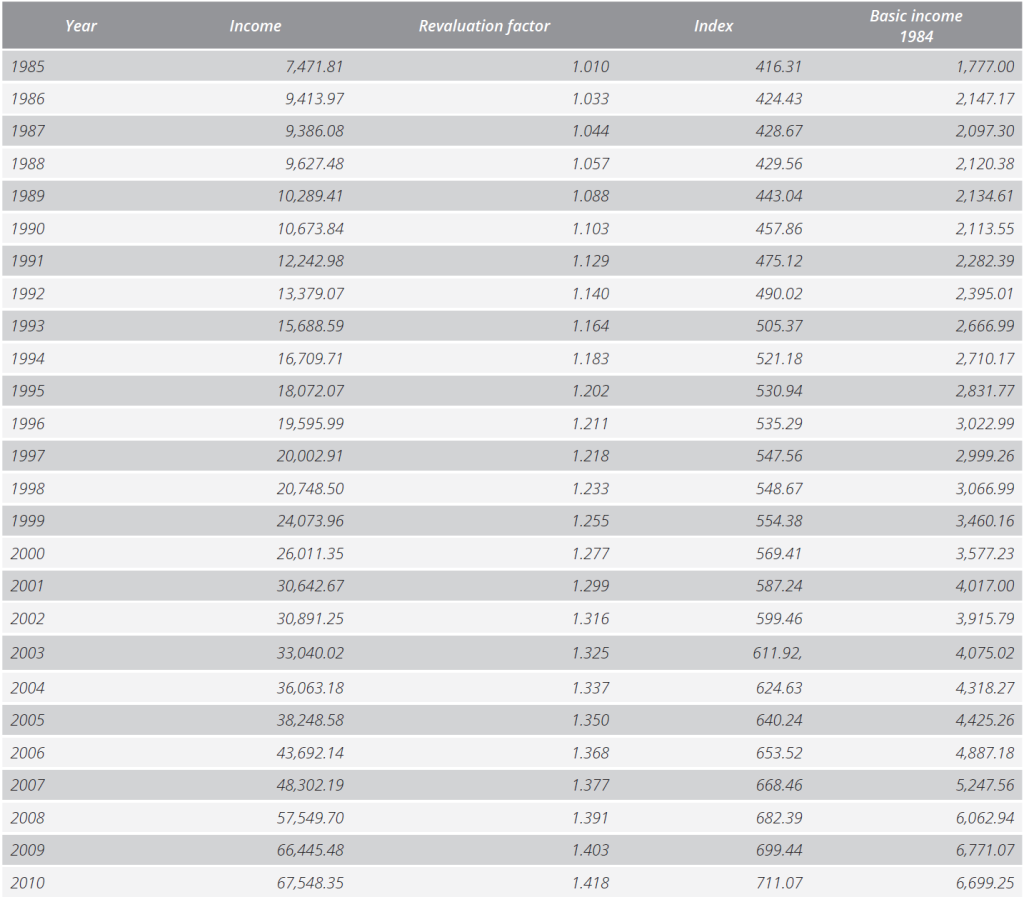

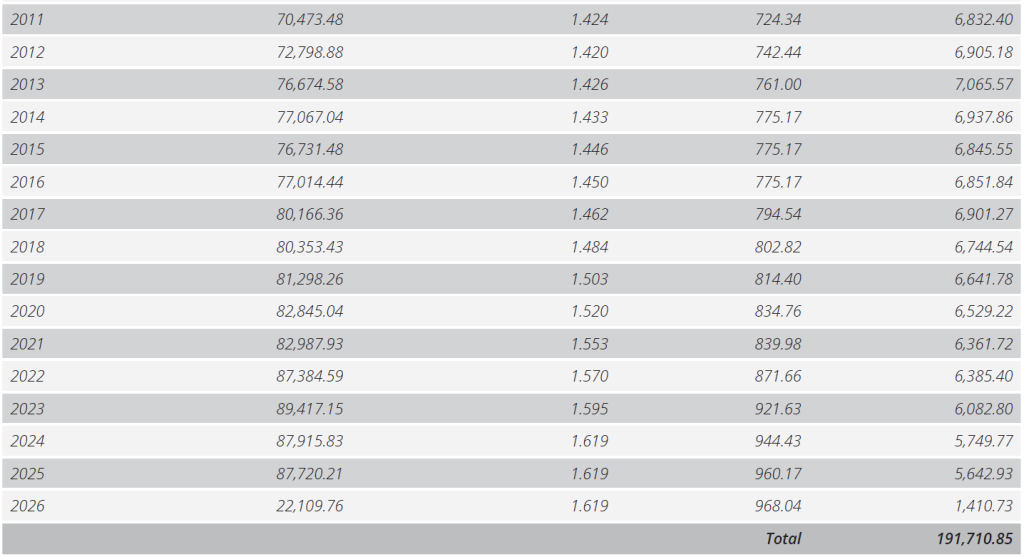

Mr. Schmit was born on 1 May 1969. He started working on 1 February 1985. His professional career was as follows:

Explanation: for each year, we take the income Mr. Schmit received, divide it by the revaluation factor to bring it back to the 1984 base and divide it by the index to bring it back to index 100. At the end, we calculate the sum of all annual incomes.

On 1 May 2026, Mr. Schmit turns 57 years old. At that time, he has already worked for more than 40 years. He has 483 months of compulsory insurance periods. Mr. Schmit is therefore entitled to an early old-age pension at the age of 57.

The amount of Mr. Schmit’s pension is calculated as follows:

First, we calculate the amount for the base year 1984. Mr. Schmit has a full career, so he receives all the flat-rate increases, i.e. 25.075% of €2,085, i.e. €522.81.

In addition, there are the proportional increases. Mr. Schmit benefits from the increase in the rate of proportional increases because of his age and length of membership.

The increase is equal to 0.032% (0.016% x 2; since age + career – threshold = 57 + 40 – 95= 2).

The rate of proportional increases is therefore equal to 1.763% + 0.032% = 1.795%. Therefore, the proportional increases amount to:

1.795% of €191,710.85 = €3,441.21.

The annual pension based on 1984 at index 100 is therefore €522.81 + €3,441.21 = €3,964.02.

Per month, this is equivalent to €3,964.02/12 = €330.34 index 100 and basis 1984.

To get the monthly pension amount at the 2026 standard of living and the current index, it must be multiplied by the corresponding revaluation factor and index.

As of 1 January 2026, the applicable revaluation factor is 1.57 and the index is 968.04.

The monthly pension is therefore €330.34 x 1.57 x 9.6804 = €5,020.58.

(Last updated on 19.01.2026)

What are the minimum and maximum old-age pensions?

How is the minimum pension determined?

No old-age pension may be less than 90% of the reference amount (set at the number 100 of the cost-of-living index on 1 January 1948 and for the base year 1984, at €2,085 per year) if the insured person has covered at least one 40-year period of compulsory insurance, continued insurance, optional insurance, retroactive purchase periods or complementary periods. If the insured person has not completed this 40 year period, but has 20 years of insurance for the same periods, the minimum pension is reduced by 1/40 for each missing year.

In January 2026, the minimum monthly pension of an insured person with 40 years of membership is €2,376.62 (index number 968.04 and revaluation factor 1.57). The minimum pension of an insured person with 26 years of membership is €1,544.80 (26/40 of €2,376.62).

No personal pension can be higher than 5/6 of 5 times the reference amount (fixed at the number 100 of the cost-of-living index on 1 January 1948 and for the base year 1984, at €2,085 per year). In January 2026, this is equivalent to a monthly amount of €11,002.88 (index number 968.04 and revaluation factor 1.57).

The lump-sum child-rearing allowance is granted to a parent who has devoted himself or herself mainly to the rearing of a legitimate, legitimatised, natural or adopted child (aged less than 4 years at the time of adoption), domiciled in Luxembourg and effectively residing there at the time of the child’s birth or adoption. From 1 January 2009, the condition of domicile and residence no longer applies to persons covered by a bilateral or multilateral social security coordination instrument (cross-border workers).

In order to be entitled to the lump-sum child-rearing allowance, the recipient’s pension or that of his or her spouse must not include any baby-years for the child for whom the payment is requested.

The lump-sum child-rearing allowance is also awarded to any person who has reared the child in place of the parents.

In the event of a dispute as to the beneficiary, the lump-sum child-rearing allowance shall be awarded to the parent who has been responsible for the child’s upbringing for the longest period.

In accordance with the European rules, the lump-sum child-rearing allowance should be treated as a pension component, whereas it is granted in addition to the components resulting from the taking into account of years of child-rearing as part of pension insurance. The principles laid down for pensions therefore apply, with the

consequences that this implies: personal entitlement for persons covered by the scope of the Regulation and the possibility of exchange. It must be concluded that cross-border workers may receive the benefit as part of their pension, both for the purposes of entitlement and calculation. However, as this is a personal right, survivors are excluded.

Since 1 January 2011, the lump-sum child-rearing allowance is available from the age of 65 (and not from 60 as before).

However, people who were entitled to the lump-sum child-rearing allowance on 1 January 2011 will continue to be entitled to it, regardless of whether they have reached the age of 65.

Withdrawal of the pension means withdrawal of the lump-sum child-rearing allowance.

(Last updated on 16.05.2023)

How much is the amount?

The lump-sum child-rearing allowance is €86.54 per month per child. It is subject to the social security and tax charges applicable to pensions.

(Last updated on 16.05.2023)

What is the procedure?

Applications for the granting of the lump-sum child-rearing benefits shall be addressed to the National solidarity fund. Applicants are required to provide all the information and data deemed necessary to determine under what conditions a lump-sum child-rearing allowance have been met.

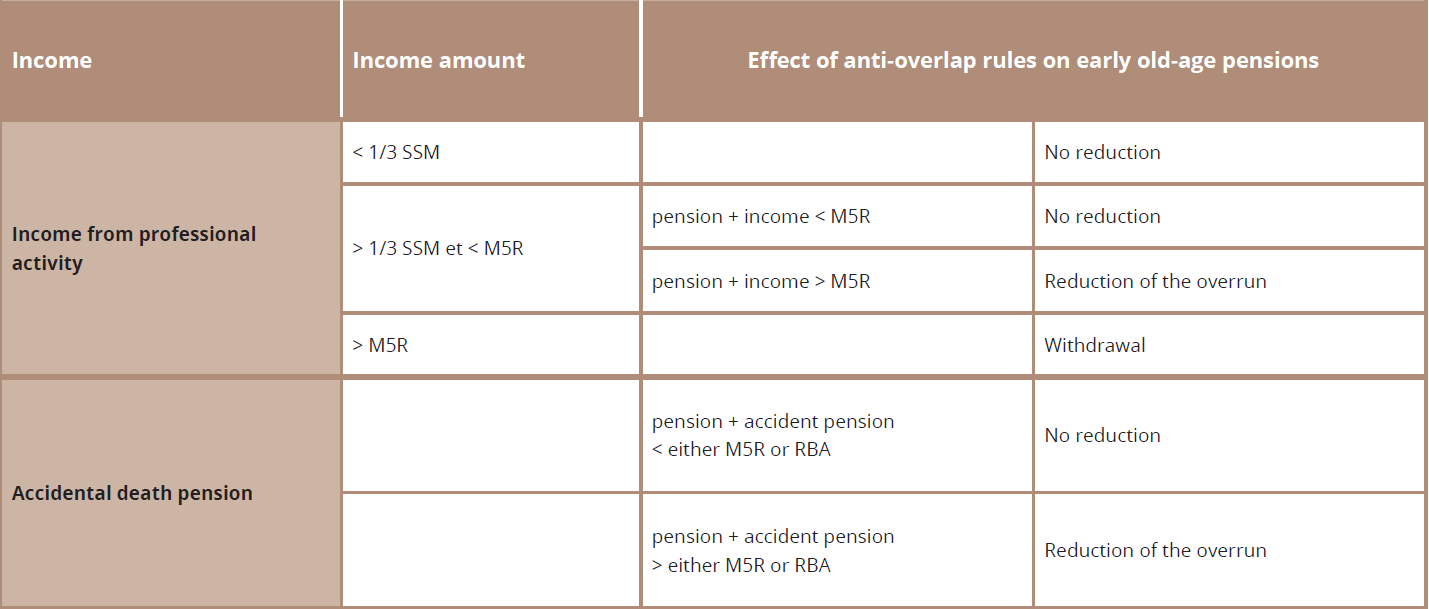

What happens if an old-age pension combined with other income?

SM: social minimum wage (salaire social minimum); RBA: income used as a basis for calculating the accident pension; M5R: average of the 5 highest salaries or incomes during the insurance period (this average cannot be less than the reference amount increased by 20% in the case of an accident pension or by 50% in the case of paid employment) Source: CNAP

What about combining a normal old-age pension with other income?

Luxembourg law allows pensioners over 65 to work in any occupation. They can therefore freely combine their old-age pension with an income.

(Last updated on 16.05.2023)

What about a combination of an early old-age pension and employment?

The beneficiary of an early old-age pension may only engage in insignificant or occasional paid employment. Insignificant or occasional activity is considered to be any continuous or temporary activity generating an income in Luxembourg or abroad which, spread over a calendar year, does not exceed 1/3 of the social minimum wage per month. On 1 January 2026, the monthly social minimum wage is €2,703.74; 1/3 of this amount is equivalent to €901.25.

Thus, a recipient of an early old-age pension whose salary, spread over a year, does not exceed 1/3 of the social minimum wage per month, will not have a reduced pension.

On the other hand, anti-overlap provisions are applied if the gross salary, spread over a calendar year, exceeds 1/3 of the social minimum wage per month. There are three possible cases:

If combining the early old-age pension with a salary results in exceeding a ceiling set at the average of the 5 highest annual contributory incomes during the insurance period, the pension is reduced by the difference between the sum of the salary and the pension and the ceiling of the 5 highest incomes, if the pension alone is lower than this ceiling. This ceiling may not be lower than the reference amount plus 50% (€ 3,961.04 per month on 1 January 2026).

Example

(For the sake of simplicity, the calculations are made for the month of January 2026. In fact, all amounts are taken into account at their value reduced to index 100 on 1 January 1948 and determined for the base year 1984. The income combined with the pension is reduced to the base year level by dividing it by the revaluation factor and the index).

The recipient of an early old-age pension continues to receive a monthly salary of €2,500 for 12 months, which amounts to €30,000 per year.

Let’s assume that his monthly pension, calculated without any reduction provision, amounts to €2,600 or €31,200 per year.

Let’s also assume that the average of the 5 highest incomes of the insurance period amounts to €50,000 at the index number of 1 January 2026.

The salary received is more than 1/3 of the social minimum wage.

Total salary and pension therefore amount to €61,200 (€31,200 + €30,000).

The combined annual pension and annual salary exceed the average of the 5 best salaries of the insurance period by €11,200 (€61,200 – €50,000).

This amount is therefore deducted from the pension of our insured person who continues to receive €20,000 per year (€31,200 – €11,200), i.e. €1,666,67 per month.

If the pension is already above the ceiling, it is reduced by the amount of the salary earned.

In our example, if the insured person had a pension (without a reduction provision) of €60,000 per year, it would be reduced by €30,000. Our insured person would continue to receive €30,000 a year in pension (€60,000 – €30,000), or €2,500 a month.

Finally, when earnings exceed the ceiling, the pension is denied or withdrawn.

Note that in the case of a mixed career (in Luxembourg and abroad), the ceiling of the 5 best salaries is prorated according to the length of insurance in Luxembourg in relation to the total career.

In order to save you from having to deal with the rather complicated provisions of the Social Security Code, CSL has developed a software program, available on its website, which automatically calculates the amount of the early old-age pension in case of combination with a salary.

What about a combination of an early old-age pension with self-employment?

The Social Security Code stipulates that in cases where an early retirement pension is combined with income from self-employment exceeding one-third of the social minimum wage, the pension is suspended. However, the Constitutional Court ruled that this fundamental distinction between income from salaried employment and income from self-employment violates the principle of equality before the law. Following this ruling, the CNAP now applies the same anti-cumulation rules to both self-employed individuals and salaried workers.

The early old-age pension is only recalculated once a year on 1 April. Apart from this automatic revision, a recalculation takes place in the following cases:

if the beneficiary’s professional income increases by more than 25%;

at the request of beneficiaries if they offer proof of a reduction in their income of at least 10% over 3 months;

when beneficiaries resume or abandon their professional activity.

The anti-overlap provisions remain valid until the completion of the 65th year. From then on, early old-age pensions become normal old-age pensions and are no longer subject to the anti-overlap provisions. The wages or income earned during the period of the early old-age pension are then taken into account and used to determine the proportional increases anew.

(Last updated on 16.05.2023)

What about a combination of an old-age pension and an accident pension?

If an old-age or early old-age pension is combined with an accident pension, the pension shall be reduced to the extent that it exceeds, together with the accident pension:

the average of the 5 highest annual incomes during the insurance period, without this average being less than the reference amount increased by 20% (€3,168.83 per month on 1 January 2026);

the professional income used to calculate the accident pension, if this other method of calculation is more

favourable.

There are three kinds of withholding that are generally made from old-age pensions:

Health insurance contributions

For old-age pensioners affiliated to the National health fund, the contributions are shared equally between the insured persons and the National pension insurance fund. The contribution is only intended to finance benefits in kind, as a cash sickness benefit is no longer granted. In 2023, the contribution payable by pensioners amounts to 2.8% of the gross pension.

Contribution to long-term care insurance

It amounts to 1.4% of the pension, after the deduction of 1/4 of the social minimum wage (€ 2,703.74/4 = €675.93, as of 1 January 2026).

Taxes

Pensions are subject to personal income tax. A scale of tax deductions on pensions is published annually by ministerial order. This scale can be consulted on the website of the Direct tax administration where it is also possible to calculate the income tax and the various withholding taxes on wages and pensions.

Where, a person who turns 65 and is not eligible for an old-age pension and has not received pension benefits on the basis of the periods of insurance concerned in Luxembourg or abroad, any contributions the person paid into his account, excluding the part borne by the public authorities, shall be reimbursed to him on request, taking account of the adjustment to the cost-of-living index. Such reimbursement shall result in the loss of any entitlement to benefits.

If, as a result of several activities or benefits subject to insurance, an insured person’s totalcontribution base exceeds the maximum contribution limit, the difference is not taken into account for calculating the pension. On the other hand, the insured person is entitled to reimbursement of the excess contributions upon request, per calendar year and at the latest when the pension is awarded.

If the holder of a normal old-age pension is employed, he is entitled to a refund of the contributions paid after turning 65, provided he submits a refund request. The refund consists exclusively of the part of the contributions paid by the insured person and is not adjusted to the cost-of-living index. The refund can be requested for each calendar year.